By Christine DiGangi

By Christine DiGangi

With big changes coming to the mortgage industry at the beginning of next year, many consumers will want to evaluate their homebuying plans. Regulations drafted by the Consumer Financial Protection Bureau will change the definition of a qualified mortgage for any loan applications received on and after Jan. 10, and many consumers may find themselves unable to meet the new requirements.

Qualified mortgages are loans that meet certain standards designed to ensure that borrowers are highly likely to be able to pay back the amount in question. Facing this challenge, it's up to the hopeful homeowner to improve their chances of mortgage approval by doing the necessary research, improving their credit profiles and meeting the qualified mortgage standards well in advance of filling out loan applications.

It's important to meet qualified mortgage standards because government-sponsored enterprises, known as GSEs, like Fannie Mae and Freddie Mac have said they won't buy non-qualified mortgages starting next year, said Joshua Weinberg, senior vice president of compliance with First Choice Lending/Bank. Fannie and Freddie don't lend to homeowners directly, rather they purchase mortgages from banks and then bundle them into securities and sell those securities to investors.

For lenders that originate mortgages with the intention of selling them to the GSEs, as many do, originating non-qualified mortgages won't be feasible. Other lenders own the mortgages they originate, meaning they don't have to worry about selling them to GSEs, and such larger portfolios could probably take on non-qualified mortgages.

What's Changing? Mortgages must pass tests of sorts to meet the standards of a qualified mortgage: The APR must be within 150 basis points (1.5 percentage points) of the annual prime offer rate, the loan term cannot exceed 30 years, points and fees cannot exceed 3 percent of the loan balance and there can be no negative amortization or interest-only payments. Under these conditions, the mortgage qualifies for safe harbor, meaning the lender is not at risk of being sued by a borrower who is unable to repay the loan.

There's a class of loans called higher-priced qualified mortgages, in which the APR exceeds the 150 basis-point limit, and in those cases, the loan falls under rebuttable presumption, meaning the lender is assumed to have complied with ability-to-pay requirements, unless a borrower or attorney argues otherwise. Loans with rebuttable presumption will likely come at an additional premium, said Cameron Findlay, chief economist at Discover Home Loans, though the price of that premium is unclear at this point.

The ability to repay comprises a series of requirements that must be met by the borrower and verified by the lender, including income and debt levels. All of these CFPB regulations are aimed at protecting consumers from mortgages they can't reasonably expect to repay, because such faulty loans triggered the recent financial crisis. Given these limitations, and some new restrictions on lenders that also go into effect in January, some have suggested that consumers may find themselves struggling to acquire a mortgage.

Weinberg described it this way: Originating a mortgage has been a process that blends science and art. The science includes the regulations that give clear guidelines for what does and does not meet qualified mortgage standards. The art comes in when an originator decides to approve or deny a mortgage application, even if a borrower doesn't meet every requirement in the book, because his or her experiences can give important context to a case that numbers and rules cannot.

"With this QM rule we're seeing an elimination of the art and a focus on the science," Weinberg said. "The way the points and fees will be calculated is now a pretty defined standard. My gut says because of the shrinking art component and the emphasis on the science, fewer people are going to qualify for loans."

While the new regulations are beyond consumer control, there are several things potential homeowners can do to prepare for buying residential property in 2014.

1. Ask Questions: If this all sounds a bit confusing, don't worry. You're not alone. Both Findlay and Weinberg acknowledged the complexity of the new rules and said there's confusion among lenders. For potential homeowners who don't understand what these changes mean for them, there's no shame in asking someone to explain them.

There are a lot of components to mortgages that first-time homebuyers may not be familiar with. Say a lender instructs you to reduce your debt-to-income ratio — that means how much of your income is tied up in student loan payments, collections accounts, judgments and other existing loan obligations. You've just learned that points and fees can't exceed 3 percent of the loan balance, but what's a point?

A point, for the record, is prepaid interest on the loan, with one point equal to 1 percent of the loan. If a borrower would rather have a lower interest rate than the one they're offered then they can pay points to lower that rate.

There's bound to be something that confuses the borrower, and no one should enter into such a large financial decision with uncertainty. Ask a lender to explain it to you, but understand that the lenders are nailing down the new processes, as well. "It doesn't bode well for the consumer when there's this confusion," Findlay said.

It's important to shop around for mortgages, and consumers should know that they can concentrate their mortgage search into a few weeks in order to minimize the impact on their credit scores. Inquiries are a major factor in your credit scores, and too many inquiries can hurt your credit. Mortgage inquiries made within that short period (which varies by credit scoring model) will count as a single inquiry on their credit reports, and because multiple inquiries would normally ding credit scores, this allows consumers to find the best offer without harming their credit profiles. If you want to see how inquiries are affecting your credit, you can look at your free Credit Report Card, which grades you on important credit score factors and gives you free credit scores.

2. Tackle Debt: If you have debt, you should try to reduce it, and this is true for all consumers, not just those looking to buy a house. Potential homeowners, however, should be extra motivated to conquer their debt: Under new ability-to-repay requirements necessary to attain a qualified mortgage, a borrower's debt-to-income ratio must be 43 percent or less, including the potential mortgage payment.

"Not only do we consider the debts that show up on your credit report, but we have to look at debts you may expect to pay in the future," Weinberg said, giving the examples of child support and student loans in deferment. "They are also going to need to be comfortable and aware of managing that debt. They are going to be asked questions about that."

Whether you're looking to buy a home next year or in two years, make a plan to manage debts now. It can only help.

3. Start the Paperwork: Though these new requirements impact consumers, they also affect lenders, and no one wants to be the first to screw up. The ability-to-repay measures require a lot of documentation, which will need to come from you, the applicant.

"We're really needing to get a very holistic perspective on the borrower in order to complete the analysis necessary to meet compliance," Weinberg said. Borrowers should ask a lender exactly what they'll need to provide, and in order to answer lenders' questions, they should also take stock of their credit profile.

Consumers are entitled to a free annual copy of their credit report from each of the three major credit bureaus — Experian, Equifax and TransUnion. That's three credit reports, so it's smart to review at least one before starting the homebuying process.

No one is sugar-coating these changes — they're a lot to handle. Changes are common in this post-crisis climate, so the best consumers can do is ask questions and do their part to prepare and educate themselves. "If we're making better loans, and the consumers are protected better, that's better at the end of the day," Weinberg said.

We would love to answer your real estate related questions, give us a call, text or email today!

-Steve and Sandra

Steve Hill and Sandra Brenner

Windermere Real Estate/FN

Seattle-Northwest

122502 Greenwood Ave N

Seattle WA 98133

call/text: 206-769-9577

email: stevehill@windermere.com

Check out these useful Home Search Apps:

Windermere for iPad

Windermere for Android

Check out these useful links:

BrennerHill.com

Best In Client Satisfaction

Seattle Real Estate Statistics

Windermere Housing Trends Newsletter

Our Preferred Lenders

George Runnels

Washington First Mortgage

WaFirstMortgage.com

call/text: 206-604-4545

Jackie Murphy

Cobalt Mortgage

CobaltMortgage.com

call/text: 425-260-6834

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

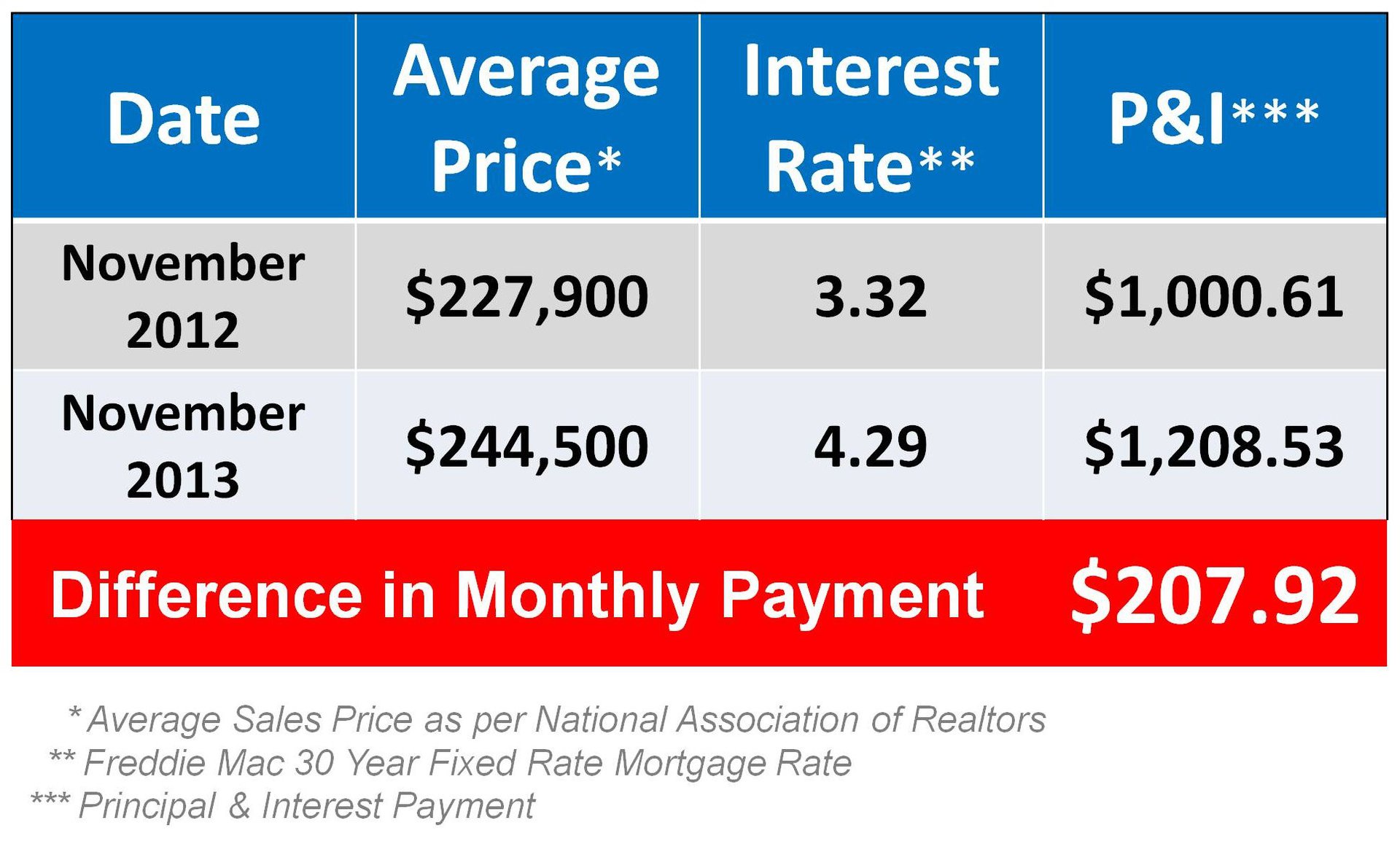

With a rise in interest rates on the horizon. How will your Buyer's Purchasing Power be impacted?

With a rise in interest rates on the horizon. How will your Buyer's Purchasing Power be impacted? Saving money is often one of the most common New Year’s resolutions. And since owning a home is easily one of the biggest expenses the average person will have in their lifetime, saving money around the home is crucial. Even for those who are able to pay off their mortgage, the cost of annual maintenance – plus the little luxuries we tack on – can really add up. In order to save some money this upcoming year on home-related expenditures, consider these steps:

Saving money is often one of the most common New Year’s resolutions. And since owning a home is easily one of the biggest expenses the average person will have in their lifetime, saving money around the home is crucial. Even for those who are able to pay off their mortgage, the cost of annual maintenance – plus the little luxuries we tack on – can really add up. In order to save some money this upcoming year on home-related expenditures, consider these steps: The price of any item (including residential real estate) is determined by ‘supply and demand’. If many people are looking to buy an item and the supply of that item is limited, the price of that item increases.

The price of any item (including residential real estate) is determined by ‘supply and demand’. If many people are looking to buy an item and the supply of that item is limited, the price of that item increases. By Christina Couch, The Fiscal Times

By Christina Couch, The Fiscal Times By

By  Check out this great link to see Snohomish County real estate statistics.

Check out this great link to see Snohomish County real estate statistics. Despite the perception that a nice home in a great location sells itself, national statistics have shown that staged homes sell in half the time of non-staged homes and for 5% more money.

Despite the perception that a nice home in a great location sells itself, national statistics have shown that staged homes sell in half the time of non-staged homes and for 5% more money. Many housing pundits are calling for home sales to do slightly better in 2014 than they did in 2013. To the contrary, we strongly believe that home sales will skyrocket with increases of 10-15% in 2014. Here are the three categories of buyers we believe will create this strong demand.

Many housing pundits are calling for home sales to do slightly better in 2014 than they did in 2013. To the contrary, we strongly believe that home sales will skyrocket with increases of 10-15% in 2014. Here are the three categories of buyers we believe will create this strong demand.